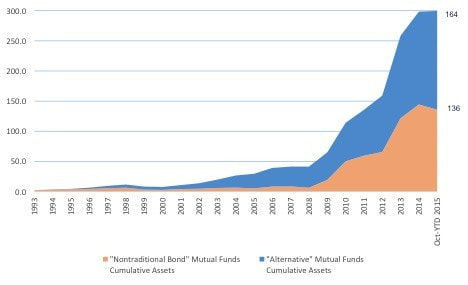

A panel session at the Inside ETFs Europe 2016 Conference examined the renewed interest in Liquid Alternatives. This article draws out and expands on some of the key findings from the panel discussion of the same title. The role of alternatives in portfolio construction The role of “alternative” asset classes in portfolio construction has traditionally been to provide differentiated asset returns that reduce overall portfolio volatility through diversification. Alternative asset classes can be broadly defined as non-equity and non-bonds, so typically includes hedge funds, property, commodities, infrastructure and private equity, and subsets of those groups. Lessons from the global financial crisis This classic Markowitz-style portfolio construction approach, based on single period mean variance optimised models was severely challenged in the global financial crisis, when diversification failed to protect assets in the short run (correlations trended to one), and risk-return opportunities became more binary (risk-on/risk-off). Assumptions challenged More specifically, some key assumptions on correlation, liquidity and time horizons that underpin portfolio construction theory required closer scrutiny. Firstly, correlations are unstable, particularly over shorter time horizons. This means that while a static approach to a diversified asset allocation may be adequate in the long run for the long run, in the short run diversification can fail to provide any protection to a portfolio. Hence the need for a tactical asset allocation approach that is dynamic. Dynamic means adapting to the fact that correlations between asset classes are different in the short run to how they are in the long run, and remain in constant flux. It’s therefore important to understand the role and correlation of alternatives to other asset classes across a time horizon that is relevant to an investor, as not all (in fact very few) investors are endowments with infinite time horizons. Secondly, liquidity matters, and matters more when needed most. While portfolio theory assumes perfect liquidity to move between asset classes, the relevance of liquidity became all too apparent in the financial crisis both from a timing perspective and a counterparty perspective. From a timing perspective, the gating of investors in certain hedge funds, and the relevance of redemption notice periods – whether daily, monthly, quarterly or annually – became all too relevant. From a counterparty perspective, solvency, capital structure and legal title became a primary concern. Finally, time horizon matters. For investors with a long-run time horizon who had no need to access capital and could weather extreme market volatility, there was sufficient risk budget not to worry about near-term correlations and liquidity constraints. But for those that needed to access capital in the near to medium term, or wished to dial-down their exposure to all risk assets in the face of potential market dislocation, these factors could not matter more. Industry response Once the dust settled, the industry response to client concerns was to consider how to offer alternative strategies (for the same diversification reasons as before), but with some hard lessons learned. Strategies had to be sufficiently flexible to be adaptive to changing market circumstances, and sufficiently liquid to be bought and sold on a daily basis. “Liquid alternatives” therefore became a buzzword for strategies that can 1) from a portfolio construction perspective, provide uncorrelated returns to traditional asset classes; and 2) from a portfolio implementation perspective, provide daily liquidity. Put differently, liquid alternatives are products that enable investors to trade “anything other than conventional beta”, according to Jean-René Giraud, CEO of Trackinsight, a European ETF research provider that is part of Koris International. Liquid Alts – delivered as mutual funds The growth in “liquid alt” was focused initially in the US mutual fund space (and were sometimes known as 40 Act funds as they were governed by the US Investment Company Act of 1940). The nature of investment strategies offered was therefore governed by what was permissible under the 1940 legislation – for example the requirement to offer daily liquidity, and to calculate a daily NAV. However, this also meant constraints around concentration, excessive leverage and short-selling. While these constraints were more restrictive than private/non-registered hedge funds, this sub-optimality was considered outweighed by investor demand for daily liquidity. Following the financial crisis, there was explosive growth in liquid alt funds, as illustrated in Fig. 1, below: Figure 1: Growth in Liquid Alt Mutual Funds (US)  Note: The chart combines the Morningstar Alternative Mutual Funds and Morningstar Non-Traditional Bond Funds sectors to represent a Liquid Alt mutual fund sector.

Source: Spouting Rock, Morningstar Direct, as at 31st October 2015. Morningstar subdivides liquid alt funds into the following sub-sectors: Managed Futures, Long-Short Equity, Multi-Alternative, Market Neutral, Nontraditional Bond, Multicurrency, Bear Market. Managers of liquid alt funds ranged from specialist boutiques to retail versions of established hedge fund managers. Growth in AUM in liquid alt mutual funds has since tapered off possibly because the liquid alt exposure is becoming more readily available – to institutional and retail investors alike – through Exchange Traded Products (ETPs). Liquid Alts – delivered as ETPs The growth in Liquid Alts continues in the ETP space which has enabled rapid innovation in the breadth and depth of the range of strategies available. With TERs of 0.20% to 0.60% for ETPs, compared to TERs of approximately 2.00% for 40 Act funds, there is a compelling cost efficiency too. This is a key reason that institutional investors are looking at liquid alt ETPs as a lower cost alternative to hedge funds with a similar portfolio function, according to Jay Pelosky of J2ZAdvisory a New York-based global investment advisory firm. The number of liquid alt (including Smart Beta) index strategies available to fulfil the role of of providing differentiated returns to traditional asset classes is expanding rapidly on both sides of the pond:

While the range of products available is far greater in the US than in Europe at this stage there is potential for Europe to “leapfrog” and catch up in terms of innovation and development given the high level of research in alternative strategies from institutional investors, index providers and academia, according to Mr Giraud. Liquid Alts – delivered as Model Portfolios Retail investors are not limited to alternative mutual funds, or alternative ETPs. Liquid Alt strategies can be made available via managed accounts which are unconstrained by the parameters of the 1940 Act or individual ETP construction. One of the key enablers for this was the investment into platform technology by North American brokerages that made Model Portfolios readily manageable, according to Suzanne Alexander of Cougar Global Investments, a tactical ETF global investment strategist focusing on portfolio construction with downside risk management. So whether as an investment strategy in itself, or an alternative part of traditional strategy, liquid alternatives are helping to redefine portfolio construction. In this respect, Europe is lagging with platform providers slow to offer ETFs, let alone ETF Model Portfolios (“EMPs"), according to Giraud. UK Platforms – ETF Ready? In the UK, platform providers remain focused on mutual funds as a way of delivering investment allocation to clients, and the bulk of investment research is skewed to fund manager research, rather than ETF research. Novia Financial is one of the few platforms to offer not only traditional fund services, but is actively seeking to improve adviser access to ETFs, through technology upgrades. Platforms that are “ETF enabled” can provide advisers the tools, products, and cost structure they need to compete on like for like terms with robo-advisers which typically use ETF Portfolios, aggregated trading, and fractional dealing to deliver low-cost scalable investment solutions. With this technological parity, advisers can then differentiate themselves on the core services that robos can’t offer: financial planning/wealth structuring (typically more material than investment allocation), face to face support and a relationship based on trust. Broadening the portfolio construction toolkit Retail investors continue to seek ways to diversify their portfolios. Institutional investors are losing patience with Hedge Funds’ lack of “value for quality” evidenced by the material redemptions from hedge funds (some $14.3bn net outflows in 1q16 alone, according to Preqin). This means there is growing demand for liquid alts both from the top down and the bottom up, according to Pelosky. Funds formerly allocated to hedge funds will have to find a home, and a reinvigorated lower cost liquid alt ETP sector could be in the running to capture part of it. Notes: Participants in the panel discussion on this topic included: Henry Cobbe, Elston Consulting (moderator) Susanne Alexander, Cougar Global Investments Jean-René Giraud, Trackinsight Jay Pelosky, J2Z Advisory NOTICES: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. This article has been written for a US and UK audience. Tickers are shown for corresponding and/or similar ETFs prefixed by the relevant exchange code, e.g. “NYSEARCA:” (NYSE Arca Exchange) for US readers; “LON:” (London Stock Exchange) for UK readers. For research purposes/market commentary only, does not constitute an investment recommendation or advice. For more information see www.elstonconsulting.co.uk Image credit: Elston Consulting. Chart credit: Spouting Rock Comments are closed.

|

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

July 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|