"Asset allocation is not everything. It's the only thing."

One of the harshest lessons of the Global Financial Crisis was that when the going gets tough, correlations trend to one, giving even diversified investors very few places to hide. It wasn't about whether or not you got burned, it was a more a question of degree. While there's a time and a place for active stock selection, from a portfolio construction perspective, it's the active management of the overall asset allocation that affects the outcome. Using ETFs for portfolio construction The growing popularity in Exchange Traded Funds is in part because of their elegance in providing broad, liquid, efficient and cost-effective market access to most major asset classes with a single trade. We now have a broad range of building blocks with which to construct a diversified portfolio. As a result, the problem for investors has shifted from "How best can I access a broad choice of markets?", to "How do I create a portfolio that suits my needs?" How many ETFs are needed to create a portfolio? To create a portfolio with too few ETFs would mean there is limited scope to create different asset allocation strategies. To create a portfolio with too many ETFs introduces additional complexity, oversight requirements, and a higher degree of trading costs if the portfolio is to be regularly rebalanced. So what is the minimum number of ETFs needed to create a well-diversified portfolio? A Strategic Core For a strategic portfolio for a UK investor with £100,000 to invest and a desire to keep trading and ongoing costs to a minimum, we believe that advisers can construct strategic asset allocation models using the following “Magnificent Seven” broad asset classes alongside cash: UK Government Bonds, UK Corporate Bonds, Global Corporate Bonds, UK Property, UK Equities, Global Equities and Emerging Market Equities. All 7 of these asset classes can be accessed through BlackRock's iShares range, mostly from their cost-efficient Core range. Importantly, these ETFs are 'cash-based' or 'physical' meaning that they actually own the underlying holdings (unlike some ‘swap-based’ or ‘synthetic’ ETFs). Liquidity and diversification The fund sizes of these ETFs ranges from approx £400m to £4bn meaning external liquidity is high. Internal liquidity is as good as the underlying securities the ETF and index holds. While investors see only seven holdings, a portfolio containing these 7 large and liquid ETF building blocks represents a diversified portfolio of some 6,901 individual securities, all of which are fully disclosed for each fund. Strategic or Tactical After creating a strategic asset allocation model, ETFs mean that tactical asset allocation changes can be executed in real-time, which can give significant implementation advantage in these volatile times. As a starting point for advisers look to provide low-cost portfolio construction, using ETF building blocks for these key seven asset classes are a helpful first step. www.elstonconsulting.co.uk NOTICE This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of date of publication and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by Elston Consulting to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Elston Consulting, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. ©2016 Elston Consulting Limited. All rights reserved. BirthStar, Elston Gamma, and Elston Strategic Beta are registered trademarks of Elston Consulting Limited. All other marks are the property of their respective owners.

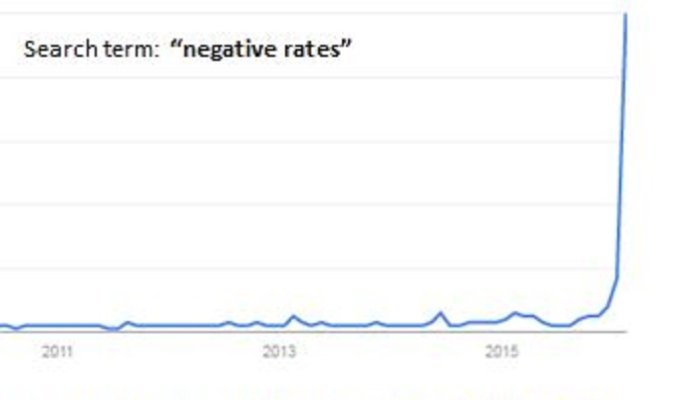

The Japanese did it. The Europeans did it. Even the educated Swedes did it. So will the Fed ever lower interest rates below zero? Markets fell out of bed last week on fears the Fed might shift from a Zero-Interest Rate Policy ("ZIRP") that alleviated the pain of the financial crisis to a Negative Interest Rate Policy ("NIRP") to keep the monetary stimulus to the economy alive. Why does it matter The "feasibility study" being undertaken at this stage is a long way from a policy announcement, but would indicate a very different interest rate path to December's announcement. This volte face alone would query the Fed's credibility. Add to that the known unknown of how markets might operate in this Through the Looking Glass world where you pay to lend money to the lender of last resort, and some basic assumptions around the supply of, and return on, capital have to be adapted. How does it "work"? The short answer is: we'll see. In theory, by charging financial institutions to sit on surplus cash, they are forced to put that cash to work, for example lending to corporates to keep their wheels turning. In this way, negative rates act as a stimulus to the velocity of money, rather than the quantum of money supply. What are the issues? Issue number one is that it turns the fundamental relationship between providers and users of capital on its head. Aside from that are the legal and technical issues around how NIRP can be implemented in any jurisdiction. But, as we have seen so far - where there's a will there's a way. The sector most vulnerable is the banking sector as negative interest rates wreak havoc on Net Interest Margins - the spread between banks' borrowing and lending rates that is the cornerstone of their profitability. Hence the rather brutal round of price discovery that took place in the banking sector as a response to this new known unknown. From negative yields to negative rates Short-term real yields on government debt (i.e. nominal yields, adjusted for inflation) went negative in 2008 during the financial crisis. Short-term nominal yields on government bonds, issued by, for example, the US and Germany, have dipped in and out of negative territory thereafter, as a safety/fear trade signaling that those investors would rather pay governments to guarantee a return OF their capital, than demand corporates to promise a return ON their capital. So economically speaking, negative yields are not new. But what is new is that negative interest rates are being adopted as a central bank policy. How have markets reacted? Markets hates grappling with new concepts where there is no empirical data from the past on which to make hypotheses. Hence the "shock" increase in risk premia despite the ostensible further lowering of the cost of capital. Renewed interest in gold is the natural reflex for those scratching their head as monetary policy grows "curiouser and curiouser". What next? Central banks are adding NIRP to the armory of "unorthodox" levers at theirdisposal to achieve orthodox aims. To what extent this new weapon is deployed will depend on the underlying development in fundamentals around growth, jobless rates and inflation targeting. Those targets set the course to which monetary policy will steer. Whether the new policy levers have more efficacy than the old remains to be seen. Baked beans, anyone? The UK's baked bean price war of the mid 1990s, provides a parallel to the topsy turvey economics of negative pricing. To gain and retain customer market share, the big three British supermarkets slashed baked bean prices to around 10p a tin. Tesco's then broke ranks and slashed prices further to 3p a tin (subject to max 4 cans per customer per day). Not to be outdone by its bigger rivals, Chris Sanders of Sanders supermarket in Lympsham, Weston Super Mare made history by selling baked beans for MINUS Two Pence (subject to max 1 can per customer per day). Janet Yellen - you now know whom to call. While it didn't alter the fundamentals of the retail sector, it did mark the end of an irrational era of skewed economics. For the optimists out there, perhaps NIRP heralds the same? Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. |

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

July 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|