[5 min read, open as pdf]

[5 min read, as pdf]

[5 min read, open as pdf]

[5 min, open as pdf]

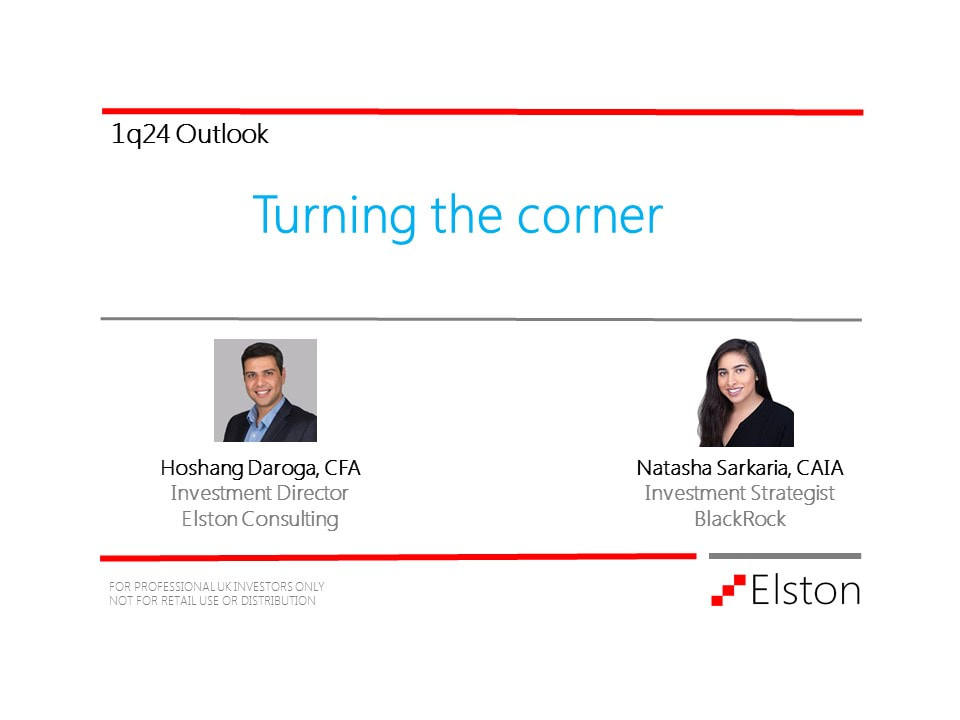

In our upcoming quarterly investment outlook, we update our key themes for 2024. Please join Hoshang Daroga (Elston Consulting) and Natasha Sarkaria (BlackRock) for this webinar.

Our key themes are: 1. Growth: Steady as she slows 2. Rates: Perfecting the pivot 3. Inflation: Ensuring portfolio resilience Our full Quarterly Investment Outlook is available to our clients. Watch the Webinar  Central Banks' policy rates are expected to pivot towards cuts in 2024 with a material impact on asset class perspectives.

Read the full article in FT Adviser

[3 min read, open as pdf]

[3 min read, open as pdf]

[1 min read, open as pdf]

[3 min read, open as pdf]

[5 min read, open as pdf]

[3 min read - open as pdf]

[5 min read, open as pdf]

[5 min read, open as pdf]

[5 min read, open as pdf]

[5 min read, open as pdf]

[5 min, open as pdf]

NMA speaks to investment consultant Henry Cobbe about positioning equities for higher inflation using sector and factor equity investing.

Listen to the podcast |

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

July 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|