[5 min read, full article in pdf]

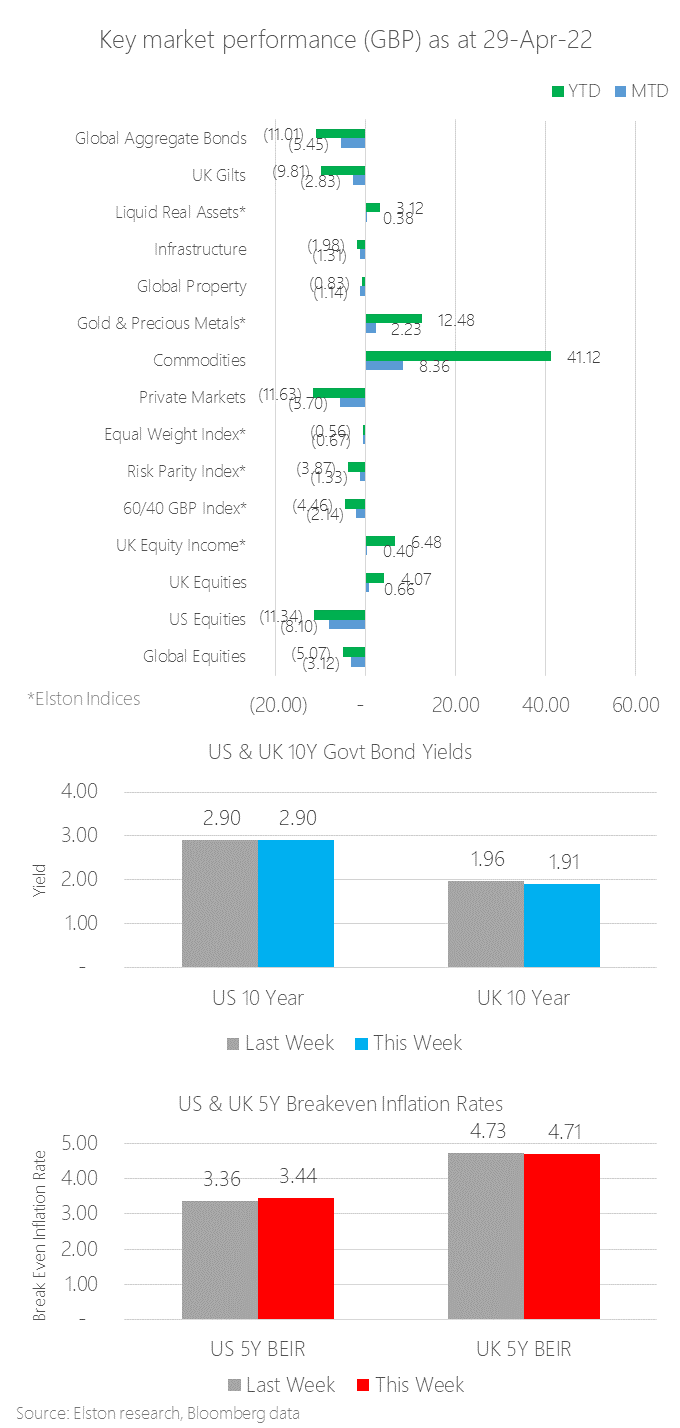

Monthly update, by exposure Once again, Commodities were the top performing asset class in April, returning +8.36% in GBP terms, owing to ongoing inflation pressure from the Russia/Ukraine war, supply-chain, sanctions and energy crisis. Gold & Precious Metals returned +2.23% as an inflation hedge. UK Equities were up +0.66%, and UK Equity Income +0.40%, compared to -8.10% for US Equities and -3.12% for Global Equities, in GBP terms. UK Equities performance was not an indicator of underlying strength, but a function of the translation effect of overseas revenues, in the context of a dramatic -4.37% decline in Sterling vs the USD – the worst decline since COVID March 2020. This came on the back of weaker retail sales and low consumer confidence. Without government spending to fill a growing vacuum, the cost of living crisis (which will only get worse in the autumn) could become recessionary in nature as consumers and businesses defer spending. This risk to growth is greater than the risk of persistently high government debt levels, in our view. Bonds continued to show they offered no place to hide with Global Aggregate Bonds down -5.45%. Our Liquid Real Assets index returned +0.38% for the month, compared to Gilts -2.83%, with comparable volatility. Within the multi-asset space, our Equal Weight index declined -0.67%, and “Equal Risk” (or “Risk Parity” Index_ returned -1.33%, compared to -2.14% for a traditional 60/40 GBP portfolio. US & UK 10 year yields closed at 2.90% (from 2.32%) and 1.91% (from 1.62%) respectively. US & UK 5 year market-implied Break Even Inflation Rates closed at 3.44% (from 3.51%) and 4.71% (from 4.72%) respectively. See full article in pdf Comments are closed.

|

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

July 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|