Investors, and indeed financial professionals and commentators, are often confused by the fact that Vanguard provides actively managed funds.

Vanguard is, of course, virtually synonymous with passive investing. It was Vanguard’s founder, Jack Bogle, who launched the first index fund for retail investors in the mid-1970s, and who has since became the most vociferous critic of active management. Yet not only does Vanguard offer active funds, it also (at least here in the UK) enthusiastically promotes them. It’s not about active and passive, Vanguard’s marketing message goes; it’s all about cost. To a large extent, that’s true. As research by Morningstar and others has consistently shown, cost is the single most accurate predictor of future fund returns. Certainly, Vanguard’s active fund fees are generally considerably lower than those of its rivals. But, given the choice of an active Vanguard fund and a passive one, which should you go for? The investment author Andrew Hallam conducted research into this question in March 2015. He looked at the performance of Vanguard’s equity and bond funds, across seven different categories, over the previous ten years. In some categories, Hallam found, the active funds produced the higher returns (particular in international equities). But, overall, Vanguard’s index funds beat the active funds by 0.71% per year. Now, 71 basis points might not sound like a great deal, but when that figure is compounded over several decades, it can add up to a substantial amount. Someone else who has looked at this issue closely is the financial adviser and author Mark Hebner. In June 2016 Hebner analysed the performance of all 60 of Vanguard’s US-based active funds which had a track record of at least ten years. The fees, he confirmed, were substantially lower than the industry average. Vanguard charged an average of 0.36% for its equity funds and 0.21% for its bond funds. Hebner then looked at turnover ratios. The average was 40% for equity funds and 90% for bond funds; in other words, a typical holding period was between one and two-and-a-half years. These figures are much more in line with the industry average and imply that Vanguard’s active managers tend to make decisions based on short-term outlooks. Although transaction costs aren’t included in the headline fee, they are borne by the investor and have a significant on net returns. The next question Hebner addressed was whether Vanguard investors could expect superior performance in return for the premium they were paying for active management. This is what he found:

This distinction between repeatable skill and random chance is very important. By random chance alone, you would expect either one or two of the funds analysed (1 in 40 to be precise) to produce what’s called statistically significant alpha. Put another way, no more of Vanguard’s funds outperformed than you would expect just from random chance. “In general,” Hebner concluded, “Vanguard has not demonstrated that their process of hiring the best analysts and managers and implementing their investment strategies is superior to anyone else. To say they apply a unique process to just two of their investment strategies seems very unlikely.” So let’s go back to our original question: Are Vanguard’s low-cost active funds a good bet? They are, as with all active funds, most definitely a bet. But a good one? Well, because the fees are lower, using an active fund from Vanguard is a better bet than choosing a typical average fund. But the bottom line is that markets are efficient. All active management, low-fee or otherwise, is a zero-sum game before costs and a negative-sum game after costs. Not even Vanguard, for all the good that it’s done for investing and for investors, is immune to those brutal facts. Do Vanguard’s active managers possess skill and insight or have resources at their disposal that active managers that all the other big fund houses don’t? The figures don’t lie, and the figures suggest they don’t.  One of the biggest attractions of having a broadly passive investment strategy is the simplicity of it. You don’t have to speculate on particular sectors or regions or constantly monitor how your portfolio is performing. The long-term market return is more than adequate to meet the need of most investors, and by simply aiming to capture that return at very low cost, you’re giving yourself every chance of a successful outcome.

Index funds themselves are beautifully simple, and so too are passively managed exchange-traded funds, or ETFs. You know exactly what you’re getting with them. But when you buy an actively managed fund you’re next quite sure. Many active equity funds, for example, include an element of bonds, cash or both, and because active managers typically turn over their entire portfolio every couple of years or so, it’s very difficult to keep tabs on everything you own at any given time. A more worrying development in recent years is that, with active managers finding it increasingly hard to beat their benchmarks, they are resorting more and more to complex strategies. Principally, these strategies come in three different forms: Leverage — in other words, the fund manager borrows money to increase the potential return of an investment Short selling — that is, the manager sells a security that they don’t own, or that they have borrowed, in the hope that the the security’s price will decline, allowing them to buy it back at a lower price to make a profit Options -- in other words, the fund manager pays for the right to buy or sell a security at an agreed price at a later date They’re often called hedging strategies; that is, they’re ostensibly designed to protect investors from risk. In practice, though, they often have the opposite effect; all three types of strategy carry a degree of risk that the end investor may not want to take. Worryingly, recent research from Canada has confirmed that active managers are making increasing use of these complex strategies, resulting in higher fees, lower returns and greater risk. The paper in question, entitled Use of Leverage, Short Sales and Options by Mutual Funds, was produced by three academics at the Smith School of Business at Queen’s University in Ontario. According to the authors — Paul Calluzzo, Fabio Moneta and Selim Topaloglu — in the 15 years prior to the paper’s publication in March 2017, 42.5% of US domestic stock funds have used leverage, short sales or options at least once. Between 1999 and 2015, the percentage of funds allowed to use all three rose from 25.7% to 62.6%. But, the researchers found, there was a price to pay for end investors for this additional complexity. Funds that used complex investments, they calculated, had a 0.59% decrease in excess return and a 0.072% increase in expenses. So, what did the researchers find specifically on risk? To quote the paper: "Although (managers) use the instruments in a manner that decreases the fund's systematic risk, they hold portfolios of riskier stocks that offset the insurance capabilities of the complex instruments. “We find not only that funds that use complex instruments take more risk, both systematic and idiosyncratic, in their equity positions, but also that bylaws that authorise complex instrument use are associated with greater fund risk.” In the paper’s conclusion the authors say this: “Our results suggest that the use of complex instruments is associated with outcomes that harm shareholders: lower returns, higher unsystematic risk, more negative skewness, greater kurtosis (essentially volatility) and higher fees. “Overall, it appears that mutual fund investors are better off choosing simplicity.” So, why is it that active managers are using these complex strategies more and more? The bottom line is that regulators have allowed them to. But you could also argue that one reason active managers are resorting to using them is that they’re increasingly under pressure to prove that they can beat the index. Put another way, active managers are becoming increasingly desperate. To quote the investment author Larry Swedroe: “The active world has to fight back to keep their share, and one way to do that is to add complexity. They need to say, ‘We have a story to tell, and you need to be a member of our secret club, which has all theses superior instruments.’” Investors should not be seduced by these sorts of marketing messages. In investing, simplicity is the ultimate sophistication, and ideally that means avoiding actively managed funds altogether.  Whilst advisers and investments are comfortable and familiar with the simple term “funds” (has anyone heard of an “CIS (Collective Investment Scheme) Conference” or being an “AUT (Authorised Unit Trust) investor”? There is much less familiarity with the once-institutional and now pervasive ETFs (Exchange Trade Funds). That lack of familiarity means that for some reason that particular TLA has stuck.

Claer Barrett in FT Weekend’s FT Money section tries to demystify the jargon – but ends up makes thing sound more complicated than they need to be. Advisers wanting to check or brush up on the difference between an ETP, ETF, ETN and ETC could do well to invest 2 hours of their time to earn accredited CPD (Continuous Professional Development) from the roadshow being run by Copia Capital Management to get a solid understanding of this increasingly popular and pervasive investment vehicle. As for civilians – customers and investors – it's actually quite simple. It’s about money. Client money. And how it gets put to work. So forget the TLAs and the alphabet soup of ET-this and ET-that. The key question to ask managers is “What are you doing for your fee, and how do I get to keep the most of my available return?” The investment management industry is waking up to the fact that its customers deserve more English-language dialogue, and fewer abbreviations. QED. NOTICES: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. This article has been written for a US and UK audience. Tickers are shown for corresponding and/or similar ETFs prefixed by the relevant exchange code, e.g. “NYSEARCA:” (NYSE Arca Exchange) for US readers; “LON:” (London Stock Exchange) for UK readers. For research purposes/market commentary only, does not constitute an investment recommendation or advice, and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product. This blog reflects the views of the author and does not necessarily reflect the views of Elston Consulting, its clients or affiliates. For information and disclaimers, please see www.elstonconsulting.co.uk Photo credit: squarespace,com; Chart credit: N/A; Table credit: N/A  John Authers’ Long View article in the FT this weekend addresses market timing. While he claims that just passive investors are such bad timers, we would go further: most are.

Attempts to time the market (choosing the right moment to buy or sell into risk assets) are a mug’s game. Great for brokerages that delight in investors’ fees levied to senselessly overtrade. Bad for investor’s portfolio outcomes. Despite the annual survey by Dalbar that investors’ attempts to time the market is really bad for their portfolio, people – including some portfolio managers – still try and have a go. The problem is that in timing the market, we become slaves to our behavioural biases around entry points, and the noise around market sentiment. An investor fearing Brexit might have – out of emotion – sold everything to cash stocked up on gold sovereigns and run for the hills whilst tracing Irish ancestry. The smart thing was to acknowledge sterling weakness and increase their allocation to FTSE100 exposure where companies have predominantly foreign earnings. So what do you do if you don’t want to time? The answer’s simple: have a rule. If you’re moving from holding one portfolio of risk assets to another (e.g. switching managers). There’s no point trying to time – switching on a relevant valuation point (e.g. month or quarter end) keeps you “in the game” and allows you to reset the performance measurement clock. If you’re moving from 100% cash to a 100% non-cash portfolio of equities and bonds, it’s slightly different: your entry point has a huge impact on long-term value of your portfolio. In this instance, I would want to “average in”, either by allocating 1/12th of the capital each month into the proposed portfolio, or a quarter of the capital each quarter. By using "pound cost averaging” - your entry point is exactly that: an average. But that’s better than flipping a coin on the vicissitudes of Mr. Market. NOTICES: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. This article has been written for a US and UK audience. Tickers are shown for corresponding and/or similar ETFs prefixed by the relevant exchange code, e.g. “NYSEARCA:” (NYSE Arca Exchange) for US readers; “LON:” (London Stock Exchange) for UK readers. For research purposes/market commentary only, does not constitute an investment recommendation or advice, and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product. This blog reflects the views of the author and does not necessarily reflect the views of Elston Consulting, its clients or affiliates. For information and disclaimers, please see www.elstonconsulting.co.uk Photo credit: Google Images; Chart credit: N/A; Table credit: N/A Private clients and families wanting wealth advice, typically want holistic wealth advice.

That's why it's worth remembering that investment capital is only one form of capital. Client fact finding should go well beyond understanding an investment portfolio, to account for other forms of capital - what it is and how it's structured. What are the other key forms of client capital to consider: Land: the oldest capital of all, since "they just don't make it anymore" - how is it held, how is it managed. In the UK agricultural yields nose-dived when the US prairies got going and crisis-related spikes aside, have never fully recovered. But "green gold" remains a resilient, and tax-efficient, store of value, and a source of collateral where productive. Property: principal, residential, and commercial property all require attention and management. Providing a store of value, an income yield and a source of collateral, it's no wonder that bricks and mortar continues to play such an important role in overall wealth. It's all the easiest "immovable" thing to tax. In the UK, taxation for properties has tightened for offshore owners, and now residential buy-to-let properties. Staying on top of the changing tax position is key for any type of property - whether owned for lifestyle or investment. Business: operating businesses can continue to provide an engine for family wealth. Again how it's owned and managed is key, as well as a picture of its capital intensity and capital requirements. How and whether returns are paid out or re-invested all form part of the broader financial landscape. Chattels: chattels are subject to their own esoteric tax treatment, and are a source of pleasure as well as a store of value. Inventorying, maintaining and insuring them are the larger headaches, with different experts needed in different fields. Trust capital: is the client a settlor or beneficiary of discretionary, life interest trust: if so, what are the terms of the trust, who are the trustees, how is it managed, and what is the tax position. Like personal capital, trust capital could simply be an investment portfolio, or itself made up of a mixture of the different types of capital outlined here. Charitable capital: whether supporting a historic, or creating a new charitable fund or trust, ensuring charitable capital is efficiently managed requires a keen eye on economies of scale. Ensuring it is properly and transparently deployed requires commensurate due diligence. Human capital: most of all, there's not much point to well-managed wealth if it can't be modeled to suit client objectives and needs - be these material or emotional. After all, you can't take it with you. Balancing this with an intergenerational view and succession plan is probably the hardest part for an adviser. So whilst there is no shortage of investment portfolio managers to choose from (and selecting, monitoring and reviewing one is another whole challenge), a holistic approach requires much greater scope and a flexible coalition of expertise. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. Additional disclosure: This article has been written for a UK audience. For research purposes/market commentary only, does not constitute an investment recommendation or advice, and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product. This blog reflects the views of the author and does not necessarily reflect the views of Elston Consulting, its clients or affiliates. For information on Elston’s research, products and services, please see www.elstonconsulting.co.uk Photo credit: Google Images; Chart credit: N/A; Table credit: N/A  "Asset allocation is not everything. It's the only thing."

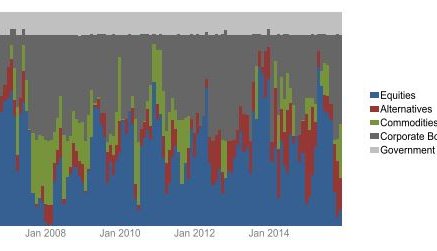

One of the harshest lessons of the Global Financial Crisis was that when the going gets tough, correlations trend to one, giving even diversified investors very few places to hide. It wasn't about whether or not you got burned, it was a more a question of degree. While there's a time and a place for active stock selection, from a portfolio construction perspective, it's the active management of the overall asset allocation that affects the outcome. Using ETFs for portfolio construction The growing popularity in Exchange Traded Funds is in part because of their elegance in providing broad, liquid, efficient and cost-effective market access to most major asset classes with a single trade. We now have a broad range of building blocks with which to construct a diversified portfolio. As a result, the problem for investors has shifted from "How best can I access a broad choice of markets?", to "How do I create a portfolio that suits my needs?" How many ETFs are needed to create a portfolio? To create a portfolio with too few ETFs would mean there is limited scope to create different asset allocation strategies. To create a portfolio with too many ETFs introduces additional complexity, oversight requirements, and a higher degree of trading costs if the portfolio is to be regularly rebalanced. So what is the minimum number of ETFs needed to create a well-diversified portfolio? A Strategic Core For a strategic portfolio for a UK investor with £100,000 to invest and a desire to keep trading and ongoing costs to a minimum, we believe that advisers can construct strategic asset allocation models using the following “Magnificent Seven” broad asset classes alongside cash: UK Government Bonds, UK Corporate Bonds, Global Corporate Bonds, UK Property, UK Equities, Global Equities and Emerging Market Equities. All 7 of these asset classes can be accessed through BlackRock's iShares range, mostly from their cost-efficient Core range. Importantly, these ETFs are 'cash-based' or 'physical' meaning that they actually own the underlying holdings (unlike some ‘swap-based’ or ‘synthetic’ ETFs). Liquidity and diversification The fund sizes of these ETFs ranges from approx £400m to £4bn meaning external liquidity is high. Internal liquidity is as good as the underlying securities the ETF and index holds. While investors see only seven holdings, a portfolio containing these 7 large and liquid ETF building blocks represents a diversified portfolio of some 6,901 individual securities, all of which are fully disclosed for each fund. Strategic or Tactical After creating a strategic asset allocation model, ETFs mean that tactical asset allocation changes can be executed in real-time, which can give significant implementation advantage in these volatile times. As a starting point for advisers look to provide low-cost portfolio construction, using ETF building blocks for these key seven asset classes are a helpful first step. www.elstonconsulting.co.uk NOTICE This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of date of publication and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by Elston Consulting to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Elston Consulting, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. ©2016 Elston Consulting Limited. All rights reserved. BirthStar, Elston Gamma, and Elston Strategic Beta are registered trademarks of Elston Consulting Limited. All other marks are the property of their respective owners.  It's hard not to get emotional when markets get difficult.

As with any temper-tantrum, having a clear rules-based approach can help maintain investment discipline when emotions run high. One of the attractions of a multi-asset Smart Beta approach is that portfolios can dynamically adapt to "reflect the pulse" of the markets following clearly defined, systematic rules. While this may be short on art, and long on science, compared to smart Alpha managers, the scientific approach also benefits from the certainty of much lower fees. Furthermore, a dynamic approach can help mitigate tail-risk. For anyone except those with an infinite time horizon (endowments), relying on a traditional single-period mean variance optimisation model for asset allocation strategy is problematic, because the long-run assumptions on which they rely do not necessarily hold for the short-run. And when it comes to managing tail-risk, the short-run matters. This is why our portfolio construction approach is outcome-oriented, aiming to create for example a Max Sharpe portfolio or Min Volatility out of a broad opportunity set of liquid, physical ETFs representing a broad range of asset classes and geographies. We've just past the 1-year live-pricing anniversary of the Elston Strategic Beta indices - the Global Max Sharpe strategy (Ticker ESBGMS) and Global Min Volatility (Ticker ESBGMV) strategy. For asset-owners looking at alternative ways to manage risk beyond a long/short 2&20 approach, low-cost risk-based multi-asset strategies are becoming a compelling alternative. |

ELSTON RESEARCHinsights inform solutions Categories

All

Archives

April 2024

|

RSS Feed

RSS Feed

Company |

Solutions |

|